Blog Detail

Take Advantage of Low Interest Rates to Get More Home for Less

May 10, 2019

Summit Homes has partnered with the Jim Alderman Team at North American Savings Bank as our preferred mortgage lender. Here are his thoughts on current interest rates.

You’ve probably heard that interest rates have dropped to historically low levels and now is a good time to buy a new home. If you’re considering buying a home in the next year, you may want to begin the process sooner than later. Today’s low interest rates can affect your purchasing power, allowing you to buy more for less.

What is your purchasing power? It refers to how far your dollar goes. In the case of buying and financing a home, purchasing power is the amount of house you can buy based on what you can afford for a monthly payment. If interest rates increase, the only way to keep the payments lower is to borrow less money, which typically means buying less home.

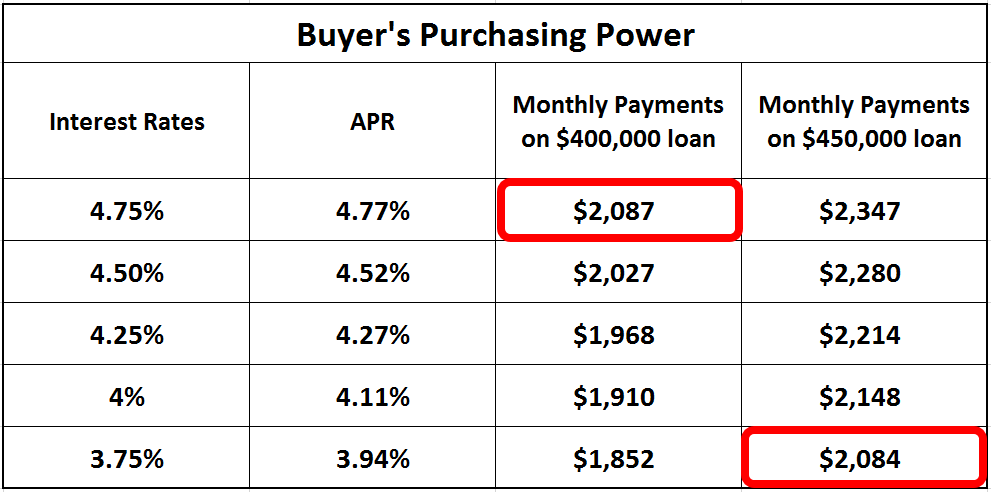

The chart below shows how different rates affect monthly principal and interest payments for two different borrowing scenarios*:

*Rates shown are based on a 30-year fixed rate, with 360 equal payments for the amounts shown. Payment amounts shown do not include amounts for taxes, insurance premiums or escrow items and that the actual payment obligation may be greater.

You can see how the buyer’s purchasing power changes based on what interest rate they can secure. A buyer who secures a rate of 3.75% for their new home could have roughly the same monthly payment ($2,087) on a $450,000 loan as someone with a rate of 4.75% would spend on a $400,000 loan. The lower the interest rate you can get, the more home you can afford.

Note - the chart above doesn’t factor in a down payment amount on the home and focuses on Principal and Interest (P&I) monthly payments. If you’re interested to see how your monthly payment may change with interest rates, you can calculate that here.

It wasn’t that long ago that rates were double if not triple what they are now. Back in 2006, the average 30-year mortgage interest rate was around 6.4%. While not much higher than today’s rates, even a few percentage points can make a huge difference in monthly payments. In 2000, interest rates were averaging around 8%. Your monthly principal and interest payments for a $400,000 loan would have been around $2,935 – almost 50% higher than the highest amount on the chart above. And in 1981, buyers faced interest rates around 16% or higher (source).

Thankfully, today you can take advantage of historically low interest rates and be armed with more purchase power. You may find that you can afford monthly payments on a larger, more expensive home. To find current rates, click here.

As a full-service mortgage banker, NASB and the Alderman Team's mission is to provide an unprecedented level of service and customized home lending experience that meets your individual needs. They have the market knowledge and expert advice to help home buyers choose the right home loan for their financial needs. Get pre-approved now!

Did you know that you get a NASB $1000 closing credit when you finance through the Jim Alderman Team when buying your Summit home? Don't miss out on these extra savings! To look at our available Move-In Ready homes, click here. Please text Ashley for more information at 816-326-2909.

Did you know that you get a NASB $1000 closing credit when you finance through the Jim Alderman Team when buying your Summit home? Don't miss out on these extra savings! To look at our available Move-In Ready homes, click here. Please text Ashley for more information at 816-326-2909.

Jim Alderman

jalderman@nasb.com

nasb.com/jimalderman

816-347-4240

NMLS #407543